Life insurance has long served as a crucial financial safety net for families and households…

The Basics of Life Insurance

Life Insurance is typically a fundamental part of a family’s financial portfolio. Despite its importance, many Americans are still not covered. The number one reason people cite not buying life insurance is due to perceived cost. Yet, 80% of Americans overestimate the cost by more than 2x.*Life Insurance helps compensate for the inevitable financial consequences that accompany the loss of life. We know it is a complex topic but with the right kind of knowledge, you can make the right choices and ensure peace of mind for yourself and your family. This blog addresses some of the basics that you need to know about life insurance.

Life Insurance is typically a fundamental part of a family’s financial portfolio. Despite its importance, many Americans are still not covered. The number one reason people cite not buying life insurance is due to perceived cost. Yet, 80% of Americans overestimate the cost by more than 2x.*Life Insurance helps compensate for the inevitable financial consequences that accompany the loss of life. We know it is a complex topic but with the right kind of knowledge, you can make the right choices and ensure peace of mind for yourself and your family. This blog addresses some of the basics that you need to know about life insurance.

A life insurance policy is a contract between an insurance company and the policyholder. Policyholders pay insurance companies their premiums for the life insurance coverage. The policyholder assigns a beneficiary or beneficiaries to the policy. The insurance company agrees to pay a claim otherwise referred to as the death benefit to the beneficiar(ies) of the policy if and when the insured person passes away.

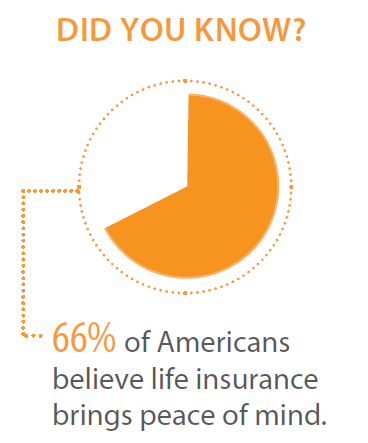

Life insurance is important if a person has people depending on him or her for financial support. Parents who have kids will buy coverage for peace of mind that their kids will not suffer financially in the event of a passing.

There are two main types of life insurance: term and permanent.

Term life insurance is typically the more affordable option. The policyholder selects the duration of time they think they will need coverage, usually 10, 20, or 30 years, and pays the premium for that period. If you have a term policy and die within the term, your beneficiaries receive the death benefit. Most term policies will either expire or the premiums will adjust significantly at the end of the term.

Permanent insurance, by contrast, provides lifelong protection. As long as you pay the premiums and no loans, withdrawals, or surrenders are taken, the full amount will be paid. Because it is designed to last a lifetime, permanent life insurance accumulates cash value and is priced for you to keep it over a long period of time.

It’s impossible to say which type of life insurance is better because the kind of coverage that’s right for you depends on your unique circumstances and financial goals. Often, a combination of term and permanent insurance is the right solution.

Typically, people with little to no adverse medical history will pay lower premiums than someone with a history of conditions such as diabetes, cancer, or health problems. Risky behaviors such as smoking, skydiving, or motorcycle racing can also contribute to higher premiums being charged by the insurance company.

Life insurance makes sure that most of the financial losses that accompany someone’s death can be taken care of. It simply takes care of obligations that require financings like funeral expenses, loans, and education for dependents. It lessens the financial strain of the remaining family members during the grieving process and long after. It is, therefore, important for the working class, business people and those who stay at home to consider.

No one enjoys talking about life insurance but having open and honest discussions about planning for the unexpected can be surprisingly awakening. When you make plans for the future don’t forget about life insurance! For information about life insurance, talk with your local agent or click here for instant quotes.

Member Benefits does not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

Sources:

www.nerdwallet.com/blog/insurance/what-is-the-difference-between-term-whole-life-insurance/

www.lifehappens.org/insurance-overview/permanent-insurance/

www.tdi.texas.gov/pubs/consumer/cb018.html

www.lifehealthpro.com/2015/08/31/42-stats-that-explain-the-life-insurance-coverage?slreturn=1470948093

www.forbes.com/sites/timmaurer/2016/01/05/10-things-you-absolutely-need-to-know-about-life-insurance/#45a70c3e3872

money.usnews.com/money/personal-finance/articles/2012/07/23/when-should-you-purchase-life-insurance

www.firstheartland.com/insure-your-love-campaign

Related Posts